What is the tax expense that would have been reported on Lally's income statement for the year ended December 31 Year 1?

An entity has 10.000 outstanding shares with a market value of US $25 each. It just paid a US $1 per share dividend. Dividends are expected to grow at a constant rate of 10%. If flotation costs are 5% of the selling price, the cost of new equity financing is calculated by the following formula.

Which of the following phases of a business cycle are marked by an underuse of

resources?

1.The trough.

2.The peak.

3.The recovery.

4.The recession.

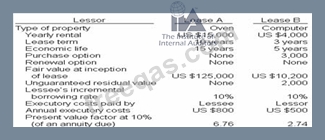

KW Ltd. leased equipment under a 4-year non cancelable lease properly classified as a finance learn. The lease does not transfer ownership or contain a bargain purchase option. The equipment had an estimated economic life of 5 years and an estimated residual value of US $20.000. Terms of the lease included a guarantees residual value of US $50,000. KW initially recorded the leased equipment at US $240,000 and its depreciation polity for owned assets is to use the straight-line method. Thus, the amount of depreciation that should be charged each year is:

CORRECT TEXT

Simulation, a widely used technique in decision modeling, is a(n):