Which of the following statements best describes an operating procedure for issuing a new Financial

Accounting Standards Board (FASB) statement?

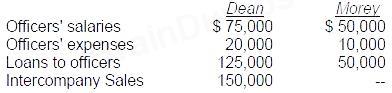

Dean Co. acquired 100% of Morey Corp. prior to 1989. During 1989, the individual companies included in

their financial statements the following:

What amount should be reported as related party disclosures in the notes to Dean's 1989 consolidated

financial statements?

In 1992, hail damaged several of Toncan Co.'s vans. Hailstorms had frequently inflicted similar damage to

Toncan's vans. Over the years, Toncan had saved money by not buying hail insurance and either paying

for repairs, or selling damaged vans and then replacing them. In 1992, the damaged vans were sold for

less than their carrying amount. How should the hail damage cost be reported in Toncan's 1992 financial

statements?

Which of the following statements is incorrect regarding the inputs that can be used to measure fair

value?

I. Level I inputs are the most reliable fair value measurements and Level III inputs are the least reliable.

II. Level I measurements are quoted prices in active markets for identical or similar assets or liabilities.

III. A fair value measurement based on management assumptions only (no market data) would not be

acceptable per GAAP.

IV. The level in the fair value hierarchy of a fair value measurement is determined by the level of the

highest level significant input.

Foy Corp. failed to accrue warranty costs of $50,000 in its December 31, 1992, financial statements. In

addition, a $30,000 change from straight-line to accelerated depreciation was made at the beginning of

1 993. Both the $50,000 and the $30,000 are net of related income taxes. What amount should Foy report

as prior period adjustments in 1993?